The Kelp-Aave Incident: What the On-Chain Data Tells Us About DeFi's Risk Infrastructure Gap

On April 18, 2026, a single misconfigured bridge verification layer triggered the largest DeFi exploit of the year. By the time Aave's Guardian completed its emergency freeze, 116,500 rsETH had been drained from Kelp's bridge adapter and used as collateral to borrow approximately $190 million in real assets. Aave's smart contracts worked exactly as designed. The problem was what they were designed to trust.

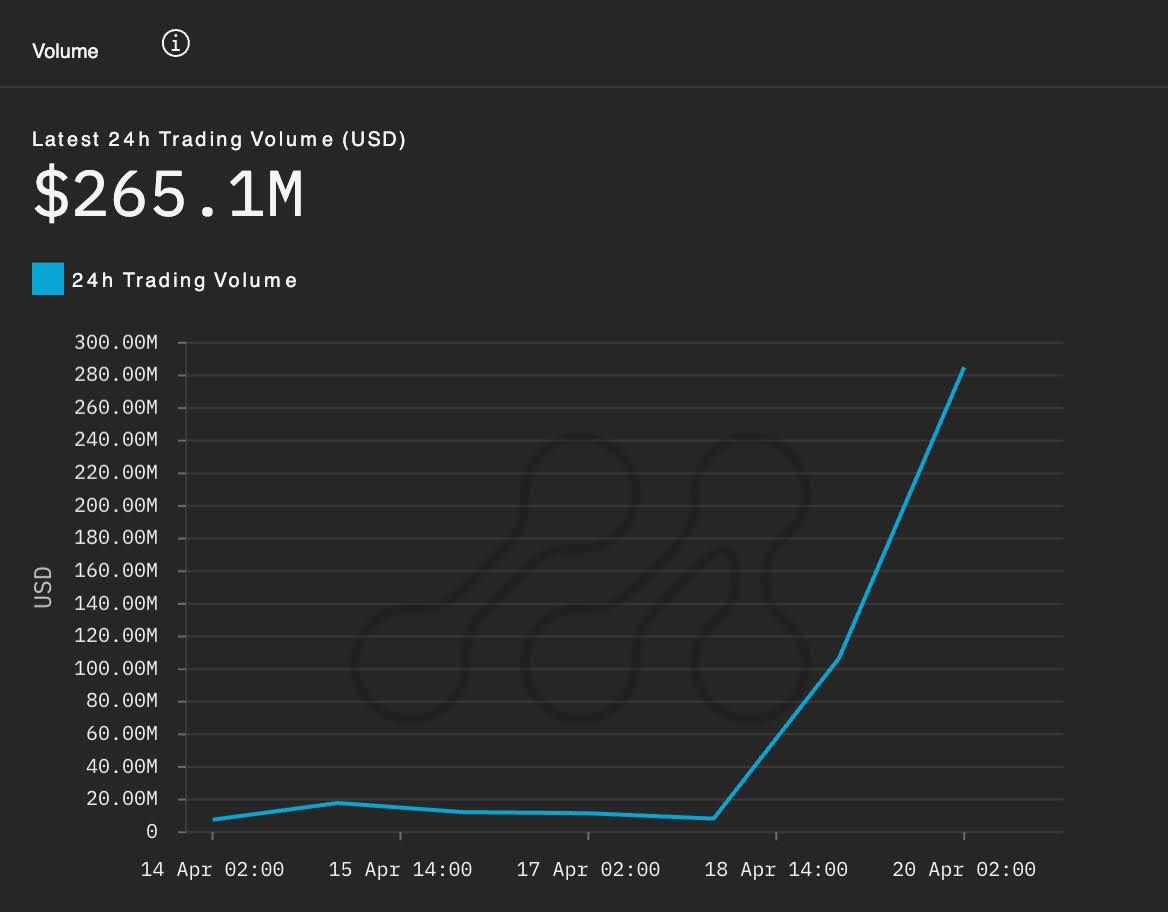

Figure 1: rsETH 24h trading volume (USD), April 14-20, 2026. Volume remained flat below $20M until April 18, then surged to $265.1M as the exploit unfolded. Source: Metrika

What Happened

Kelp DAO is a liquid restaking protocol that issues rsETH, a tradable receipt for ETH staked via EigenLayer. To move rsETH across blockchains, Kelp uses a LayerZero lock-and-mint bridge: rsETH is locked in an adapter on the Ethereum mainnet, and corresponding copies are minted on Layer 2 networks. The invariant that must always hold is that rsETH locked in the adapter is greater than or equal to the total rsETH minted across all remote chains.

On April 18, that invariant broke. Kelp's Unichain-to-Ethereum route was configured as a 1-of-1 DVN, meaning a single verifier node was sufficient to authenticate a cross-chain message. A forged packet was verified and executed, releasing 116,500 rsETH to an attacker-controlled address with no corresponding burn on the source chain. The adapter balance dropped from 116,723 rsETH to 223 rsETH in a single block. The exploit originated on L2s, not Ethereum mainnet, and its effects spread rapidly to Ethereum and wETH markets through DeFi's interconnected infrastructure.

The attacker immediately distributed the stolen rsETH across six addresses (Address 1, 2, 3, 4, 5, and 6) funded through Tornado Cash, then deposited 89,567 rsETH as collateral on Aave V3 across Ethereum and Arbitrum, borrowing approximately $190 million in WETH against it. Kelp's emergency multisig froze core contracts 46 minutes later. A second attempted drain reverted because the recipient address had been frozen in time. The stolen WETH was already gone.

The Cascade

When news broke, large depositors withdrew billions within hours. ETH pool utilization hit 100%, followed by USDT and USDC pools. Over $8 billion left the Aave protocol within 48 hours. Users who could not withdraw began borrowing against their own stablecoin deposits at a loss. Broader DeFi TVL fell by over $13 billion in two days. A single exploit in an external bridge, originating on L2, froze rsETH and wETH markets across Aave's deployments and propagated stress to pools with no direct rsETH exposure. In a notable development, Arbitrum subsequently froze $71 million in ETH tied to the exploit, marking one of the few concrete recovery actions taken in the aftermath.

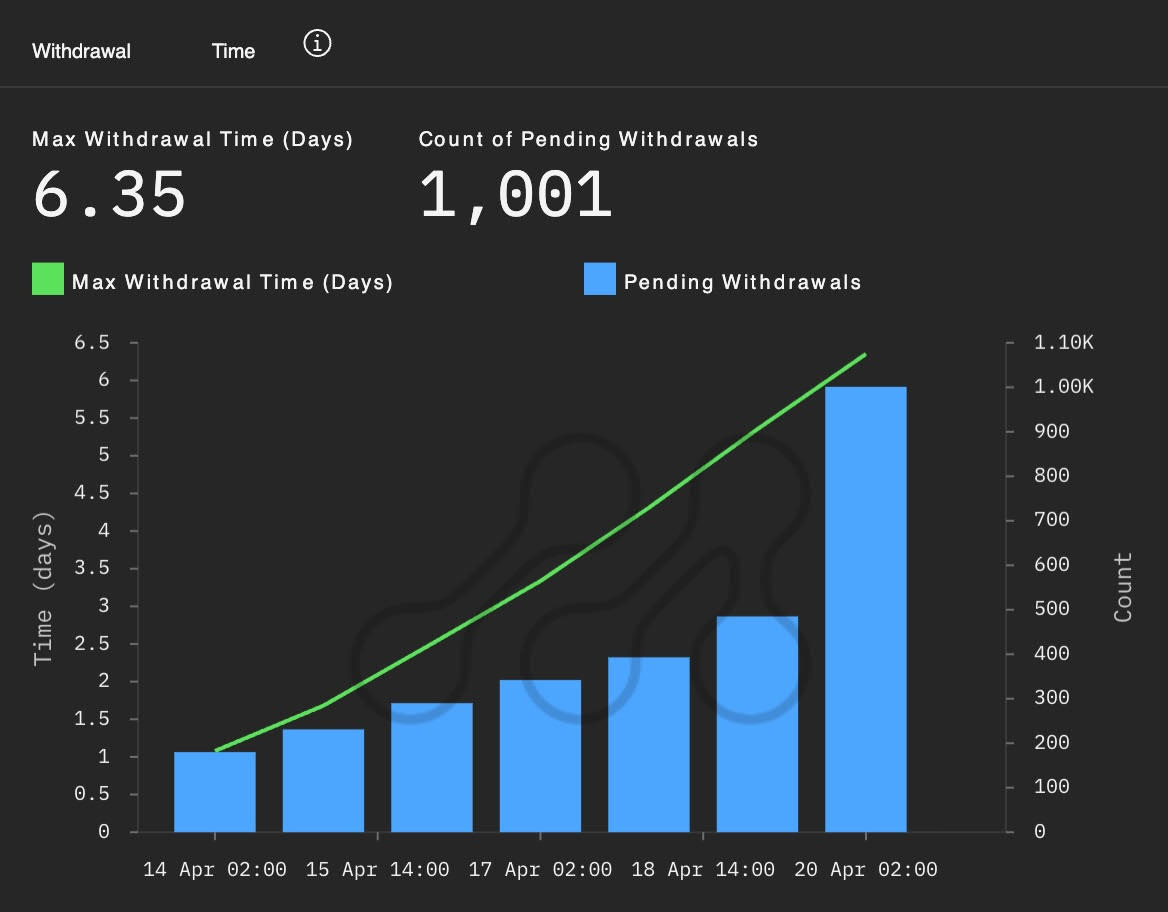

The contagion also reached stETH. Lido paused its Lido Earn product, which linked stETH and rsETH. Secondary market activity around stETH spiked to nearly 10-15x its regular volume, and withdrawal times rose from an average of 2 days to a maximum of 10 days. stETH's core TVL remained unaffected, and the amounts staked held steady, but secondary market pressure was visible and measurable in real time.

Figure 2: stETH max withdrawal time (days) and pending withdrawal count, April 14-20, 2026. Withdrawal times rose steadily from approximately 1 day before the exploit to 6.35 days by April 20, with 1,001 pending withdrawals queued. Source: Metrika

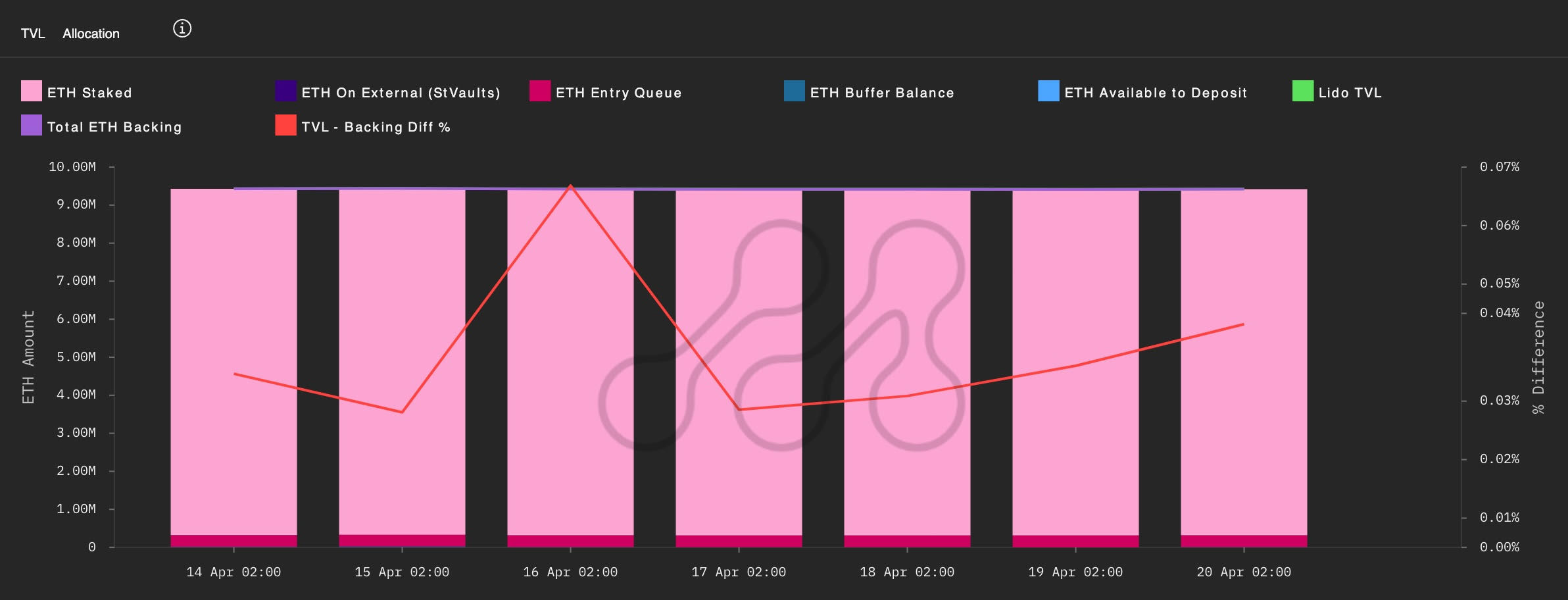

Figure 3: stETH TVL and allocation breakdown, April 14-20, 2026. ETH staked volumes remained stable throughout the incident, confirming that core protocol integrity was maintained even as secondary markets came under pressure. Source: Metrika

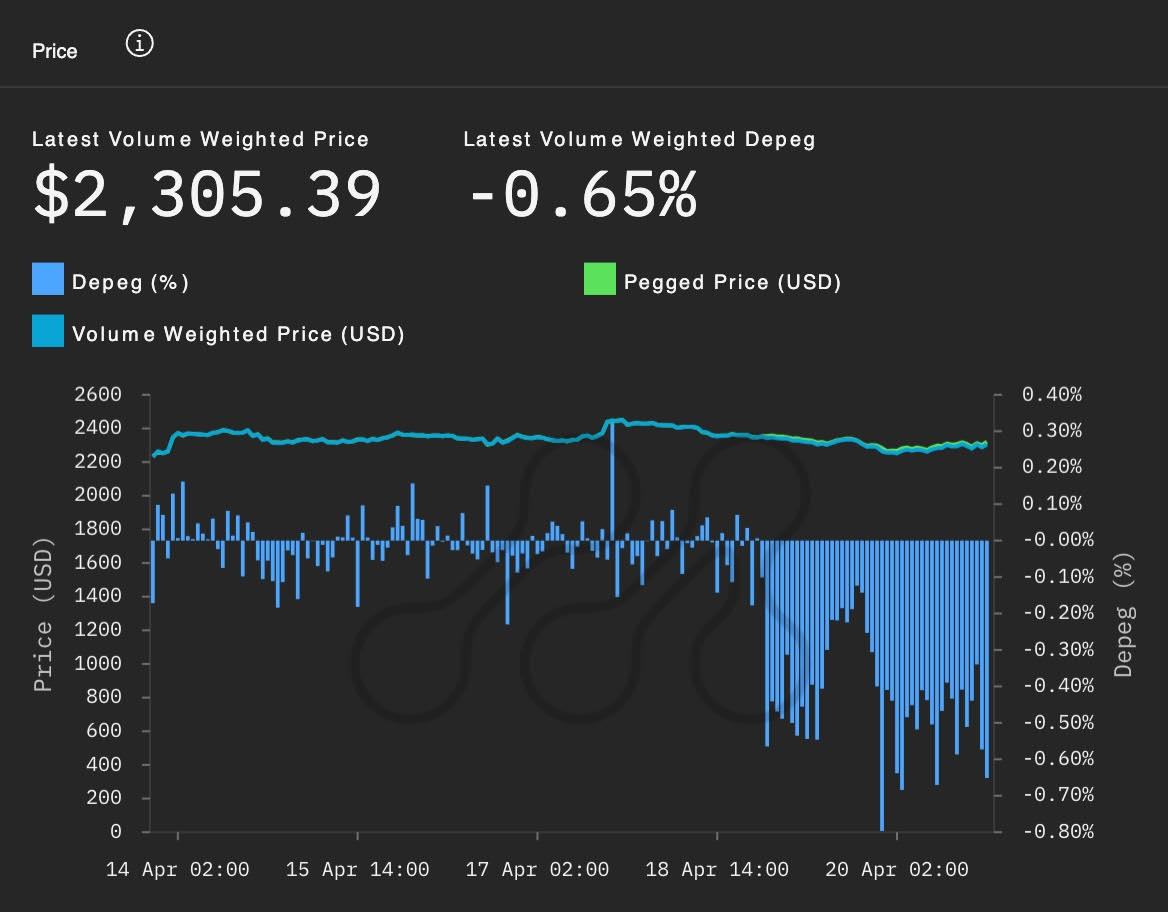

Figure 4: stETH volume-weighted price and depeg (%), April 14-20, 2026. The depeg remained within a narrow band before April 18, then deteriorated sharply, reaching -0.65% by April 20. Source: Metrika

The Bad Debt Scenarios

Kelp has not publicly confirmed how it will allocate losses. Aave's incident report outlines two scenarios. Uniform socialization across all rsETH holders results in an estimated $123.7 million in bad debt for Aave, with a roughly 15% haircut to all rsETH holders. Isolating losses to L2 holders only pushes bad debt to approximately $230 million, with Mantle facing a 71.45% WETH shortfall and Arbitrum a 26.67% shortfall. The difference is a governance decision, pending Kelp's confirmation. Kelp's treasury holds approximately $181 million. Aave's Umbrella reserve holds $54 million designated for WETH coverage. Neither alone is sufficient.

Was This Detectable?

The on-chain footprint was present. Six Tornado Cash-funded addresses received the stolen rsETH within minutes. Those addresses deposited 89,567 rsETH into Aave across seven positions over a short window, generating a sharp borrowing spike. Health factors on the attacker's positions clustered unusually close to the liquidation threshold.

No single signal would have triggered an automated halt. Aave has no per-wallet borrowing limits, no time-bound thresholds, and no native mechanism to detect whether a large collateral deposit originates from a compromised bridge. The protocol processed the transactions as valid because, by the rules it was given, they were.

What was missing was a monitoring layer capable of correlating wallet funding patterns, bridge adapter balance changes, borrowing velocity, and collateral concentration in real time. That layer does not yet exist as standard infrastructure in most DeFi deployments.

What This Means for Institutional Exposure

Three things are worth naming directly.

- Collateral risk extends beyond the protocol level. rsETH's value as collateral on Aave depended on Kelp's bridge integrity and LayerZero's verification layer. Institutions need risk frameworks that treat cross-chain infrastructure as part of the collateral stack. Part of what made rsETH attractive was its yield, 4.5% APY on top of standard ETH staking returns before the exploit. That yield reflected the layered risk that end users were taking on, much of which was not visible in standard protocol-level diligence.

- Composability amplifies tail risk. WETH represents nearly 40% of all outstanding borrows on Aave. A collateral failure in one chain's rsETH market cascaded into frozen markets and borrowing pressure across pools with no direct exposure to rsETH. Risk models built around isolated protocol analysis will consistently underestimate tail exposure.

- Governance moves slower than markets. Aave's rsETH and wETH markets were frozen on April 18, cutting off supply and borrowing. Users with positions in adjacent pools found their exit windows constrained by the mechanics of a protocol-wide freeze response. For institutions that need predictable exit windows, that distinction is material.

The signals were visible on-chain. Acting on them in time requires infrastructure that translates raw on-chain data into institutional risk signals in real time. Closing that gap is the industry's most pressing open problem.

What Real-Time Monitoring Would Have Shown

Metrika's risk analytics layer tracks precisely the signals that preceded this cascade: bridge adapter balances, borrowing velocity, and collateral concentration.

On April 18, the Kelp adapter balance dropped from 116,723 rsETH to 223 rsETH in a single block. Six newly funded addresses deposited 89,567 rsETH into Aave across seven positions within minutes. WETH borrowing utilization spiked sharply in a narrow window. Each of these was a visible on-chain event.

For institutions with real-time monitoring configured across these data streams, the window for action existed. Forty-six minutes passed between the drain and Kelp's contract freeze, and hours more before Aave's liquidity pools hit 100% utilization. The question April 18 answered is whether the infrastructure to use that window was in place. For most market participants, it was not.